New Projections Anticipate a Slowdown in Household Growth and Housing Demand

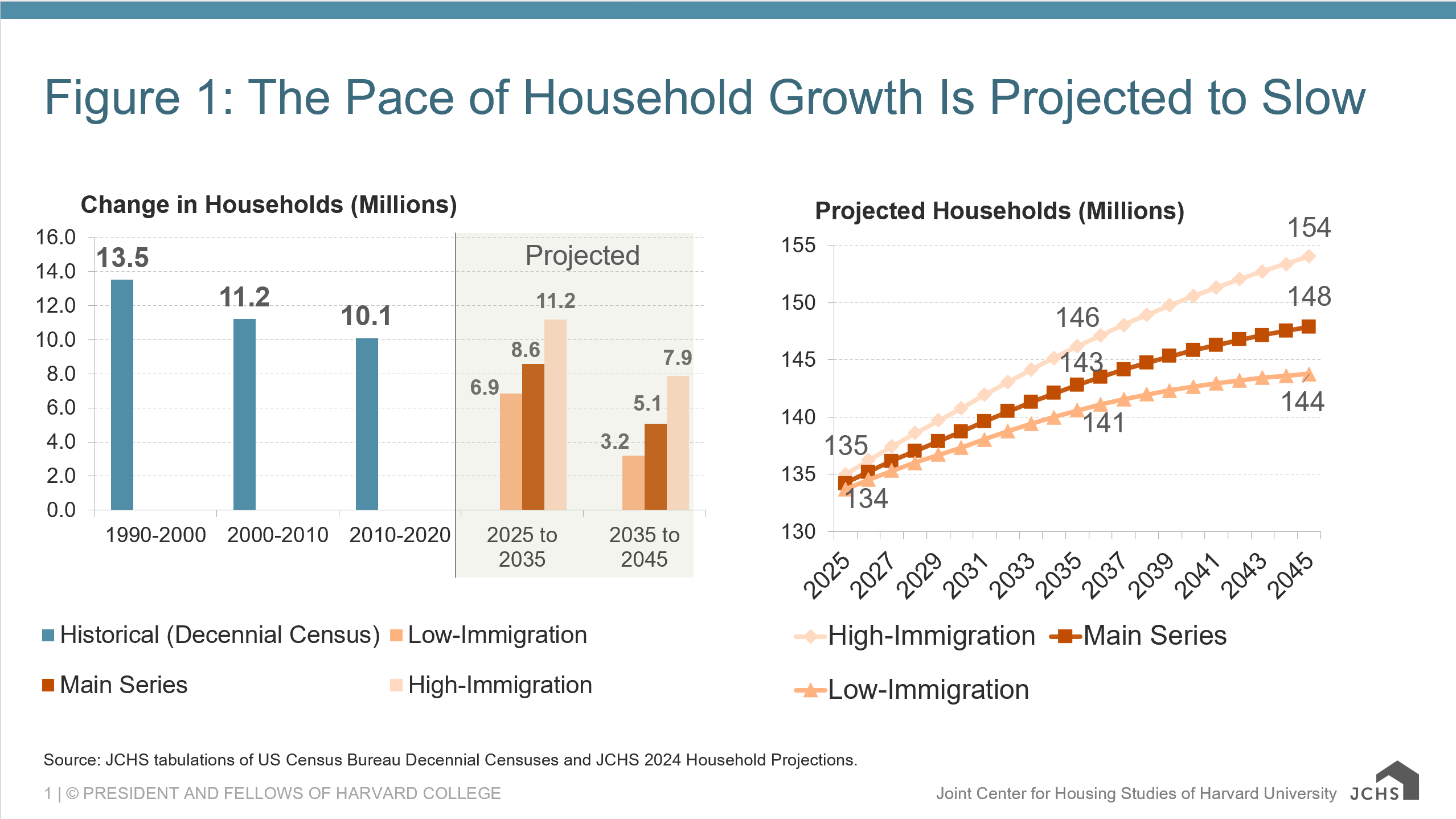

According to the Center’s new projections, the number of households in the US is expected to increase by 8.6 million, or approximately 860,000 per year between 2025 and 2035. This would be far less growth in the next ten years than in recent decades, including the sluggish 10.1 million households added in the wake of the Great Recession in the 2010s (Figure 1). The pace of growth is expected to slow between 2035 and 2045 to a gain of just 5.1 million households, which would be less growth than in any decade of the last 100 years.

Figure 1: The Pace of Household Growth is Projected to Slow

Source: JCHS tabulations of US Census Bureau Decennial Censuses and JCHS 2024 Household Projections.

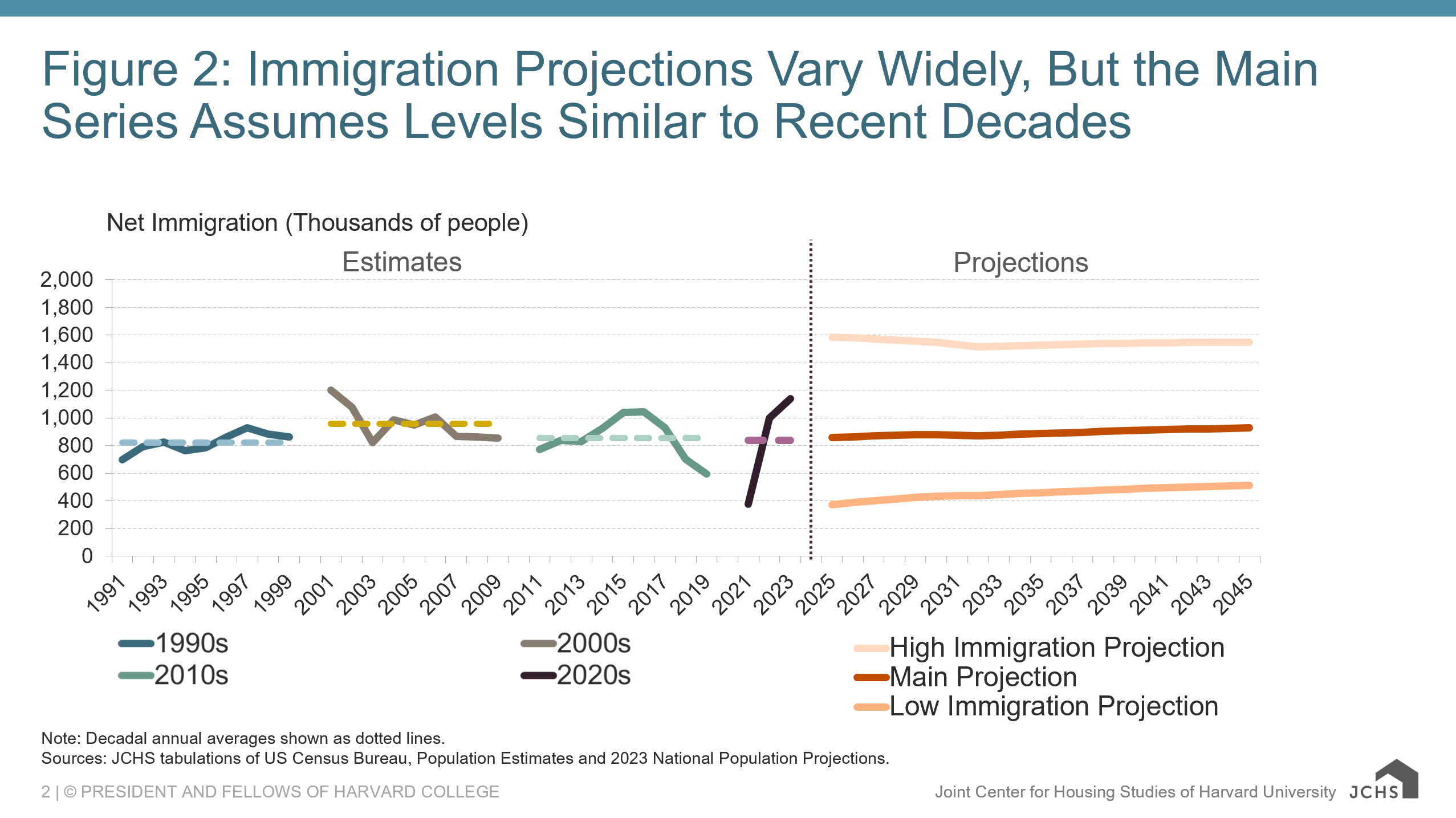

Levels could be even lower depending on immigration. Indeed, the projections are based on a scenario where immigration levels remain similar to those of the past three decades, at approximately 870,000 per year in 2025–2035 (Figure 2). A low-immigration scenario, where net gains in population from immigration fall to roughly half of their historic average over the next ten years (422,000 per year in 2025–2035) results in an increase of 6.9 million households in 2025–2035 before falling to 3.2 million additional households, or just 320,000 per year in 2035–2045.

Figure 2: Immigration Projections Vary Widely, But the Main Series Assumes Levels Similar to Recent Decades

Note: Decadal annual averages shown as dotted lines.

Sources: JCHS tabulations of US Census Bureau, Population Estimates and 2023 National Population Projections

In addition to documenting the slowdown in household growth, the projections describe expected changes in household demographics, including how new households formed by younger generations will increase the racial and ethnic diversity of US households. One of the most significant trends, however, is the growth in the number of older adult households. With the oldest baby boomers turning 80 in 2026, the number of households headed by a person aged 80 or older will rise nearly 60 percent in the next ten years—an increase of nearly 6 million households (Figure 3). This will lead to an unprecedented number of older adult households, an extraordinary need for housing and services, and ever higher numbers of households lost each year from aging or mortality that will drive down net household growth.

Figure 3: Rapid Growth in Households Aged 80 and Over and in Middle Age Groups

Source: JCHS 2024 Household Projections – Main Series

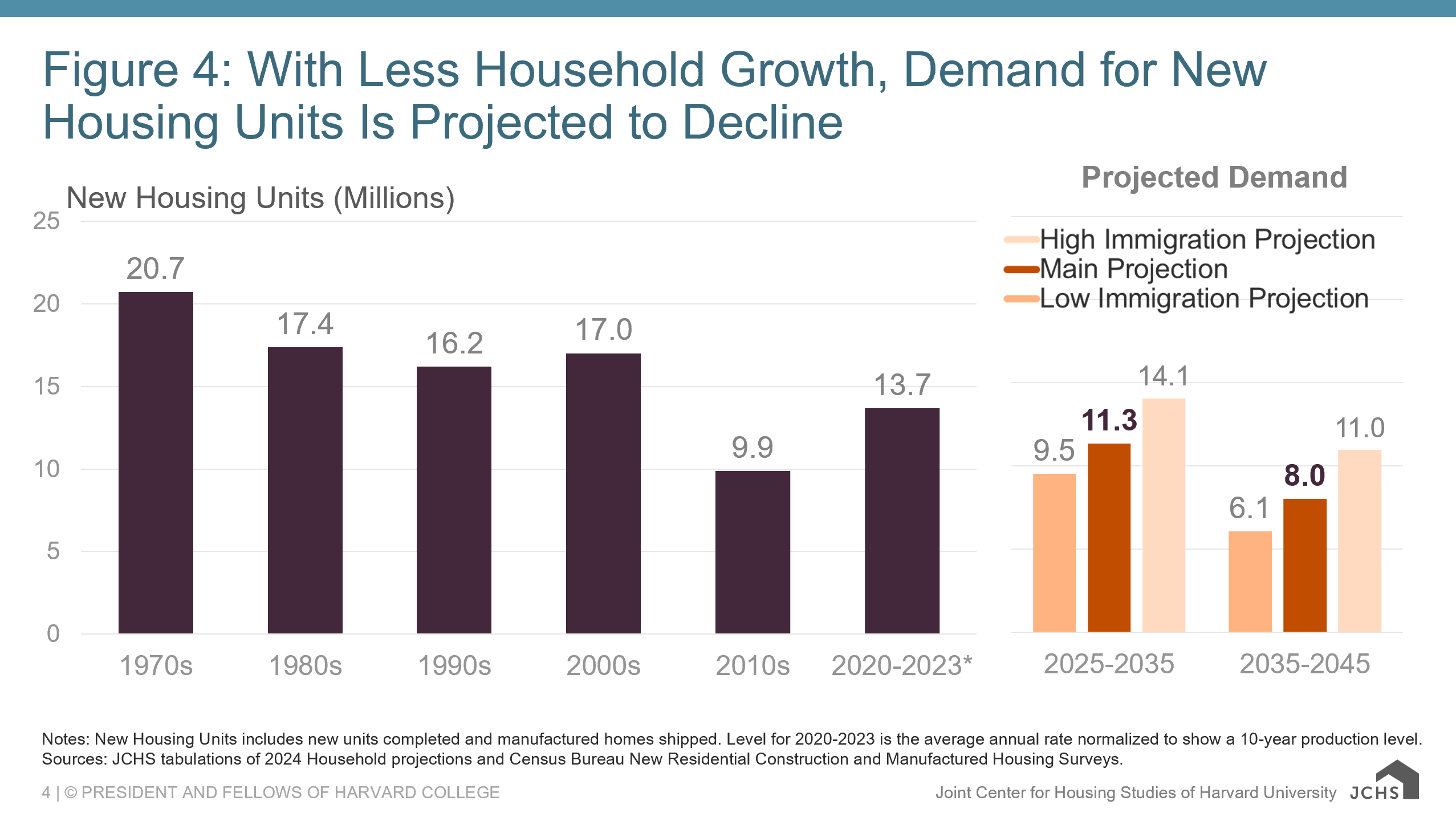

Another implication will be lower demand for housing construction. Household growth is the single biggest source of demand for new housing, along with the need to replace older homes, meet the demand for second homes, and accommodate a normal level of vacancies in a larger housing market. The projected slowdown will reduce demand for new unit construction from the current rate of 1.4 million units per year to an average of 1.1 million units per year in 2025–2035 and to 800,000 units per year in 2035–2045 (Figure 4). In the low-immigration scenario, demand would support the construction of just 950,000 new units per year in 2025–2035 and 610,000 per year in 2035–2045. These levels are well below the 1.6 million to 2.1 million units built on average each year from the 1970s through the 2000s, and nearer to the 990,000-unit annual average from the 2010s, which was a historically low decade.

Figure 4: With Less Household Growth, Demand For New Housing Units is Projected to Decline

Notes: New Housing Units includes new units completed and manufactured homes shipped. Level for 2020-2023 is the average annual rate normalized to show a 10-year production level.

Sources: JCHS tabulations of 2024 Household projections and Census Bureau New Residential Construction and Manufactured Housing Surveys.

Actual construction levels in the future could exceed these estimates to the extent that new construction is needed to overcome an existing shortage of housing, which is estimated to be anywhere from 1.5 million to 5.5 million units. If construction exceeds demand to make up for shortages in the next ten years, then actual construction levels could be higher than these projections. Beyond units needed to address the current shortfall, however, the underlying trend is for slowing demand for new units.

In sum, the projections detail a future in which the number of households grows far more slowly than previously experienced. The slowdown will be driven mainly by an increased number of older adult households that are lost or consolidated each year. Households will still form, many of them by a more diverse set of younger adults, but not enough to outweigh the rising number of households lost. The alternative scenarios show how immigration levels may temper the slowdown or accelerate it. Ultimately, less household growth will mean less demand for new housing construction, while aging of the population will put new demands on the housing stock.